Latest News

Blask: US prediction market demand rises 5x since August 2025

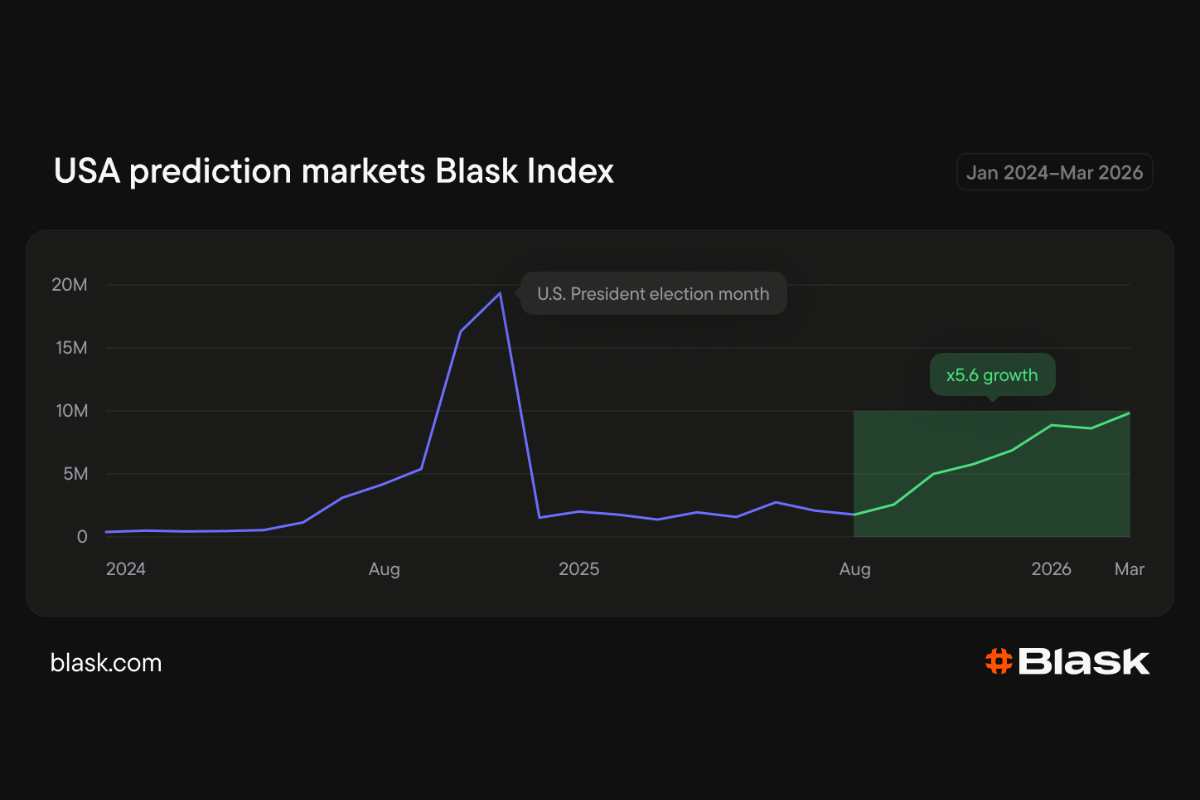

Branded demand for prediction markets in the United States has increased more than fivefold since August 2025, according to new data from Blask. The company said the rise has been sustained over eight consecutive months and comes without a single major macro event driving the category.

Blask said current demand remains about 49% below the all-time high recorded during the November 2024 US election cycle, which it described as a spike “largely driven by a single, high-impact event.” The current pattern, by contrast, suggests steadier engagement rather than an event-led surge.

The competitive landscape is increasingly concentrated. As of March 2026, Polymarket and Kalshi jointly account for around 94% of all branded demand in US prediction markets, Blask said, with both platforms gaining share during the expansion.

At the state level, Blask reported wide swings in the balance between the two leaders. Kansas is the most lopsided, with Polymarket at 95.5% of branded demand versus Kalshi’s 3.5%. Louisiana is closest, with Polymarket at 59% and Kalshi at 35.3%. Blask said California leads overall demand with 15.9% of total US branded demand, followed by New York at 10.8%.

Outside the top two, the rest of the market accounts for about 6% of branded demand, Blask said. Myriad holds under 1%, while Robinhood is the fastest-growing name tracked, with a year-over-year increase of +983.4% but a 0.24% share.

Alongside the data, Blask said it has launched a dedicated prediction market analytics feature to let operators track demand, competitive positioning and regional distribution in real time.

The post Blask: US prediction market demand rises 5x since August 2025 appeared first on Eastern European Gaming | Global iGaming & Tech Intelligence Hub.

Central America

FeedConstruct takes exclusive data and streaming rights for Nicaragua’s Liga Primera

Deal covers worldwide distribution of Liga Primera and Copa Primera content for sportsbooks and betting suppliers.

FeedConstruct has acquired exclusive worldwide streaming and data rights for Nicaragua’s top-tier football competitions, Liga Primera and Copa Primera.

The company said the agreement delivers start-to-finish coverage of every match across both competitions and expands its Central American football portfolio for sportsbook operators and providers using its data integration and streaming.

Ani Isakhanyan, Head of Rights and Content at FeedConstruct, stated, “Securing these exclusive rights is a highly valuable addition to our portfolio. Liga Primera and Copa Primera deliver the consistent football content that the global iGaming industry demands. This acquisition ensures our partners can offer comprehensive coverage of a rapidly emerging betting market.”

Allan J. Chamorro, Managing Partner at Apollo Sports Business Group, added, “Nicaragua has rapidly established itself as one of Central America’s fastest-growing football markets, attracting growing regional recognition and international commercial interest. Our partnership with FeedConstruct builds on that momentum by expanding the global distribution of Liga Primera and Copa Primera while powering sustainable commercial opportunities that strengthen clubs, elevate the competitions, and accelerate the long-term growth of the game.”

Liga Primera and Copa Primera are the main competitions in Nicaragua’s professional football calendar. FeedConstruct said the competitions are gaining regional recognition in Central America, supported by regular participation in CONCACAF tournaments.

The post FeedConstruct takes exclusive data and streaming rights for Nicaragua’s Liga Primera appeared first on EE Gaming | Global iGaming & Tech Intelligence Hub.

The UAE Lottery has partnered with SmartLife Foundation to support outdoor workers during the UAE summer, backing the Cool Bus Shelter initiative in Abu Dhabi on July 20, 2026.

The programme aligns with the UAE’s Midday Break rules, which require outdoor work to stop between 12:30 PM and 3:00 PM during peak heat. As part of the initiative, air-conditioned buses were stationed near labour sites to provide workers a place to rest before returning outdoors.

Volunteers from The UAE Lottery and SmartLife Foundation provided cold towels, cold water and drinks, according to the organisations. Workers also received portable rechargeable neck fans intended to provide additional cooling after the break.

Suzan Kazzi, Associate Director – Corporate Social Responsibility at Momentum- The UAE Lottery, said: “Outdoor workers are the backbone of our cities’ urban development, and initiatives like the Cool Bus Shelter ensure they receive the care and recognition they deserve during the most challenging months of the year. This is our small way of saying thank you and reminding them that their wellbeing truly matters”.

Abhijeet Oak, Vice President at SmartLife Foundation, added: “At SmartLife Foundation, we believe that protecting the wellbeing of outdoor workforce is a shared responsibility. Through the Cool Bus Shelter initiative, we are proud to collaborate with organizations such as The UAE Lottery and other community partners to create moments of comfort, appreciation and human connection that leave a lasting impact”.

The post The UAE Lottery backs Cool Bus Shelter initiative for outdoor workers appeared first on EE Gaming | Global iGaming & Tech Intelligence Hub.

Bally’s Intralot

Intralot Ireland Limited Signs Seven Year Contract Extension with Premier Lotteries Ireland

Bally’s Intralot announced that its subsidiary Intralot Ireland Limited has signed a seven year contract extension, through November 2034, with Premier Lotteries Ireland (PLI). The agreement supports PLI’s continued operation of the Irish National Lottery through the remainder of its license period and reinforces Bally’s Intralot’s role as a trusted technology and services partner.

Under the terms of the agreement, Bally’s Intralot will modernise PLI’s technology ecosystem by deploying its next-generation LotosX Omni solution and PlayerX Player Account Management platform. The solution will provide a modern, cloud-based technology foundation supporting lottery operations across retail and digital channels, while incorporating advanced retailer management, instant games management, device management and content management capabilities. The agreement also includes comprehensive support and maintenance services, along with cloud operations and cybersecurity services for the first year, designed to ensure the long-term reliability, security and performance of PLI’s technology environment.

Through this partnership, Bally’s Intralot will support PLI in delivering a future-ready operating environment designed to enhance operational efficiency, accelerate innovation and strengthen player engagement. The modernisation will provide a secure, scalable and resilient platform that enables PLI to continue evolving its offerings while improving time-to-market implementation of new initiatives, along with maintaining the highest standards of reliability and service to players and retailers across Ireland.

“We are pleased to extend our partnership with Bally’s Intralot, a relationship built on trust, commitment to excellence, and shared ambition since 2014. As we look to the future, this agreement provides a strong platform for continued innovation and growth, ensuring we can deliver a modern, secure, and world-class National Lottery that places responsible play at its heart while continuing to benefit communities across Ireland,” said Cian Murphy, CEO of PLI.

Robeson Reeves, CEO of the Bally’s Intralot Group, said: “We are proud to extend our long-standing partnership with Premier Lotteries Ireland for a further seven years. This agreement reflects the strength of our technology and the trust we have built with PLI over more than a decade of collaboration. We look forward to continuing to support the National Lottery of Ireland and to delivering innovative, responsible gaming experiences to players across the country.”

The post Intralot Ireland Limited Signs Seven Year Contract Extension with Premier Lotteries Ireland appeared first on EE Gaming | Global iGaming & Tech Intelligence Hub.

-

ESPN Networks3 days ago

ESPN Networks3 days agoTHE 57th ANNUAL WORLD SERIES OF POKER® CONCLUDES AN EXTRAORDINARY SUMMER OF GLOBAL ENGAGEMENT AND ELITE COMPETITION

-

Latest News7 days ago

EveryMatrix’s Fantasma Games launches three-reel slot Bonus Bullets

-

Latest News5 days ago

Booming Games launches Tasty Bonanza Max Scatter slot

-

Latest News6 days ago

SCCG Management Launches Dedicated SCCG Brazil Division with Local Partner Thomas Carvalhaes

-

Latest News7 days ago

Blokotech adds Wicked Games slots in new content deal

-

Latest News6 days ago

Esportes Gaming Brasil takes two ClienteSA Awards 2026 wins; exec named Personality of the Year

-

Canada5 days ago

Peter & Sons launches full game portfolio in Alberta

-

Canada6 days ago

ThrillTech secures AGCO supplier licence for Ontario launch