Canada

Rivalry Announces Record Fourth Quarter, Year-End 2022, and All-Time High Quarterly Revenue In Preliminary Q1 2023 Results

Rivalry Corp., an internationally regulated sports betting and media company, today announced its financial results for the three and 12-month periods ended December 31, 2022. The Company also announced preliminary results for the three-month period ended March 31, 2023. All dollar figures are quoted in Canadian dollars.

“Our market strategy and operational excellence continues to build upon consecutive record-setting quarters, driving a strong finish to the year and a robust Q1, while simultaneously demonstrating sequential narrowing losses on our path to profitability,” said Steven Salz, Co-Founder and CEO of Rivalry. “Underpinning our growth is significant brand loyalty among the Millennial and Gen Z audience and true product innovation in online betting, enabling every marketing dollar to go further, enhancing retention, and creating a distinctly unique platform. Rivalry continues to be economically rewarded for taking an inventive approach to the betting experience and tailoring it for a demographic with unique consumption habits.”

Full-Year 2022 Financial Highlights

- Betting handle was $232.8 million in 2022, an increase of 198% compared to $78.2 million in 2021.

- Revenue was a record $26.6 million in 2022, an increase of 140% from $11.0 million in 2021.

- Gross profit was $9.8 million in 2022, an increase of $7.6 million or 349% from $2.2 million in 2021.

- Net loss for the year was $31.1 million, compared to a net loss of $24.3 million in 2021. The 2022 net loss includes $8.2 million of share-based compensation expense, a non-cash item, compared to $10.5 million of share-based compensation expense in 2021.

- The Company had $16.4 million of cash and no debt as at December 31, 2022.2

Fourth Quarter 2022 Financial Highlights

- Betting handle was $83.9 million in Q4 2022, a year-over-year increase of 237% compared to $24.9 million in Q4 2021, and up 19% sequentially from the previous record quarterly handle of $70.3 million in Q3 2022.

- Revenue was $9.4 million in Q4 2022, a year-over-year increase of 338% from $2.2 million in Q4 2021, and represented the Company’s highest-ever revenue up to that point. Revenue was up 32% sequentially from $7.1 million in Q3 2022.

- Sportsbook revenue of $7.1 million in Q4 2022 was $1.0 million higher than in Q3 2022, driven by a very strong month in October. Gaming revenue of $2.3 million was up by $1.2 million or 119% over Q3 2022, as the Company began offering a wider set of casino games on its Casino.exe platform.

- Gross profit was $5.0 million in Q4 2022, a year-over-year increase of $4.6 million from $0.4 million in Q4 2021, and up 139% sequentially from $2.1 million in Q3 2022.

- Net loss for Q4 2022 was $12.3 million. The net loss included $6.4 million of share-based compensation, a non-cash expense that is not expected to recur in future periods, as well as non-recurring spending of $1.1 million. Absent those non-recurring items, the Q4 2022 adjusted net loss was $4.9 million3, in line with a trend of narrowing losses over the past four quarters.

First Quarter 2023 Preliminary Results4

- Betting handle for the three-month period ended March 31, 2023 was $120.2 million, an increase of $80.0 million or 199% from $40.2 million in Q1 2022. Betting handle increased by $36.2 million or 43% from the previous quarterly record of $83.9 million in Q4 2022.

- Revenue for Q1 2023 was $12.0 million, an increase of $7.2 million or 151% from $4.8 million in Q1 2022, and up $2.5 million or 27% over Q4 2022 revenue of $9.4 million.

- Gross profit was $5.4 million in Q1 2023, an increase of $4.8 million from $0.7 million of gross profit in Q1 2022, and up $0.4 million or 9% from Q4 2022 gross profit of $5.0 million.

- These results were achieved with a 10% reduction in marketing spend YoY.

- Net loss was $3.5 million for Q1 2023, compared to a net loss of $6.6 million in Q1 2022.

Operational Highlights

- Rivalry obtained licences in its first two fully regulated markets, commencing gaming operations in Ontario on April 4, 2022 and in Australia on May 9, 2022.

- The Company added mobile esports to its sportsbook in March 2022, enabling customers to wager on a variety of competitive esports played on mobile devices.

- The Company entered the casino segment with its first third-party game in Q3 2022 and launched its proprietary platform Casino.exe in the fourth quarter with several additional games.

- Customer registrations increased to approximately 1.5 million by the end of Q1 2023.

- Rivalry’s creator partner network and owned media properties reached a total of 85 million followers, deepening reach, acquisition, and engagement among core target audience.

- Company brand strategy helped maintain market-leading position among next generation of bettors, with Millennial and Gen Z consumers accounting for 97% of active users in 2022.

- Esports betting continues to drive significant growth, representing nearly 90% of sportsbook handle in 2022.

- The Company expanded its casino offering in January 2023 with eight new titles including live dealer and table games, and debuted Casino.exe in its home market of Ontario in March 2023.

- On April 26, 2023, Rivalry announced a private placement for gross proceeds of up to $10 million (the “Private Placement”) with participation from key sports betting, technology, and payments stakeholders, signaling a vote of confidence in the Company’s user economics and ability to execute within this emerging vertical. The Private Placement is expected to close in one or more tranches commencing on or about May 5, 2023.

Outlook

“We have reached an inflection point in the business where the economic return of our strategy and unique position at the intersection of esports and betting has outlined a clear path to profitability,” Salz added. “We are well-positioned to scale efficiently throughout the year, with a collection of near and long-term initiatives that will contribute to our disruptive product and brand.”

Initiatives the Company expects to drive continued growth in 2023 include:

- Expanding our esports offering to deepen our core product, attract new customers, and establish the most comprehensive product globally.

- Continued evolution of our interactive Casino.exe platform and release of additional proprietary and third-party games that cater to our core demographic and further establish a betting experience unique to Rivalry.

- Continued product development, including new betting markets and proprietary platform features, to meet shifting consumption habits of Millennial and Gen Z consumers.

- Launch of a mobile app in our regulated markets to increase accessibility of our product and player acquisition.

- Geographic expansion to increase our addressable market and customer base.

- Expanded brand execution through premium content, creator partner programming, and community activations to enhance customer engagement and retention, solidifying Rivalry’s leadership position among next generation consumers.

- Continuing to grow our investor base through proactive capital markets outreach.

Powered by WPeMatico

High 5 Games, the creator of premium casino content for the land based, online and social gaming markets announced it has secured supplier approval from the Alberta Gaming, Liquor and Cannabis Commission (AGLC), extending its games beyond Play Alberta to all licensed operators in the province’s newly opened commercial iGaming market.

High 5 Games has entertained Alberta players since 2024 through Play Alberta, the province’s government operated gaming platform, where titles such as DaVinci DeluxeWays, Billionaire’s Bank, Green Machine and more have become established player favourites. With Alberta’s commercial market now open, that same proven portfolio is available to all licensed operators entering the province.

Alberta’s commercial iGaming market will be opening on July 13, 2026, making it the second Canadian province after Ontario to welcome private sector operators. Overseen by AGLC and the Alberta iGaming Corporation (AiGC), the market launched with nearly 50 registered operator brands, one of the most anticipated regulated market openings in North America this year.

The approval extends High 5 Games’ regulated North American footprint, which includes New Jersey, Michigan, Pennsylvania, Connecticut, West Virginia, Ontario, Quebec, British Columbia. Alberta players will gain access to High 5’s catalogue of player favourite titles, including DaVinci DeluxeWays, Billionaire’s Bank, Green Machine and other titles through launch partnerships with operators.

“Alberta players already know and love our games through Play Alberta, that is a head start no newcomer to this market can claim. With the open market live, every operator in the province can now offer their players the award winning High 5 titles they have been playing for years, from day one.” says Tony Singer, CEO at High 5 Games.

High 5 Games’ content is certified across New Jersey, Michigan, Pennsylvania, Connecticut, West Virginia, Ontario, British Columbia and the studio has developed more than 300 games over three decades of game making.

The post High 5 Games Expands Across Alberta’s Open iGaming Market Following AGLC Supplier Approval appeared first on Americas iGaming & Sports Betting News.

The supplier can now distribute its online casino titles beyond Play Alberta to all licensed operators in the province.

High 5 Games has secured supplier approval from the Alberta Gaming, Liquor and Cannabis Commission (AGLC), allowing the studio to supply its online casino content to all licensed operators in Alberta’s newly opened commercial iGaming market.

The company has been live in the province since 2024 via Play Alberta, the government-operated platform, where it said titles including DaVinci DeluxeWays, Billionaire’s Bank and Green Machine have become player favourites. With the commercial market now open, High 5 Games said the same portfolio can be offered across operators entering Alberta.

Alberta’s commercial iGaming market is set to open on July 13, 2026, becoming Canada’s second province after Ontario to allow private-sector operators. The market is overseen by AGLC and the Alberta iGaming Corporation (AiGC) and launched with nearly 50 registered operator brands, according to the company.

“Alberta players already know and love our games through Play Alberta, that is a head start no newcomer to this market can claim. With the open market live, every operator in the province can now offer their players the award winning High 5 titles they have been playing for years, from day one.” says Tony Singer, CEO at High 5 Games.

High 5 Games said the AGLC approval expands its regulated North American footprint, which it listed as including New Jersey, Michigan, Pennsylvania, Connecticut, West Virginia, Ontario, Quebec and British Columbia. The company said it has developed more than 300 games over three decades.

The post High 5 Games wins AGLC supplier approval ahead of Alberta iGaming launch appeared first on EE Gaming | Global iGaming & Tech Intelligence Hub.

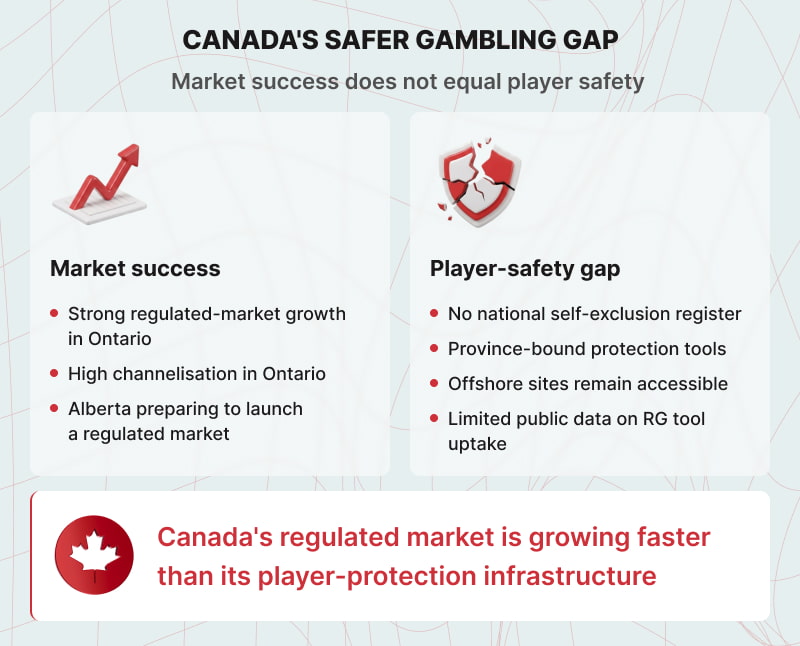

Canada’s online gambling market is the third-largest in the world. It generated approximately CAD 13.15 billion in 2025, growing faster than virtually any other country. By the metrics the industry tends to reach for, it is a success story.

Unfortunately, where many of the metrics that matter for player protection are concerned, the story is different. Unlike several other countries, Canada has no national self-exclusion register and no national licensing framework.

While Ontario is regulated, and there is a lot of excitement around Alberta opening its regulated market this summer, the overwhelming majority of online gambling in the country still happens on unlicensed platforms.

An Ontario or Alberta player who self-excludes still can gamble through offshore sites or outside the province. Canada has no single stop button.

Key Findings

- Canada has no national self-exclusion register, no national licensing framework, and the last national survey predates the legalisation of single-event sports betting.

- Offshore leakage outside Ontario ranges from 49% to 93% by province. The offshore market grew at 40% year-on-year in 2025.

- Ontario has a 91.1% channelisation rate, but 20.2% of players also play on unregulated sites.

- Player awareness of RG tools in Ontario stands at 65.4%, according to iGO’s own Leger survey baseline. No province publishes data on actual tool uptake rates.

- A CMAJ study found gambling helpline contacts in Ontario rose 198% after market privatisation, concentrated almost entirely in men aged 15 to 44.

A Fragmented System

Canada’s gambling framework is a product of its constitution. Sections 91 and 92 of the Constitution Act distribute authority to the provinces, and Section 207 of the Criminal Code permits them to conduct and manage lottery schemes within their own borders. A 1985 federal-provincial agreement completed the transfer, leaving Ottawa without a gambling regulator and the country without national standards of any kind.

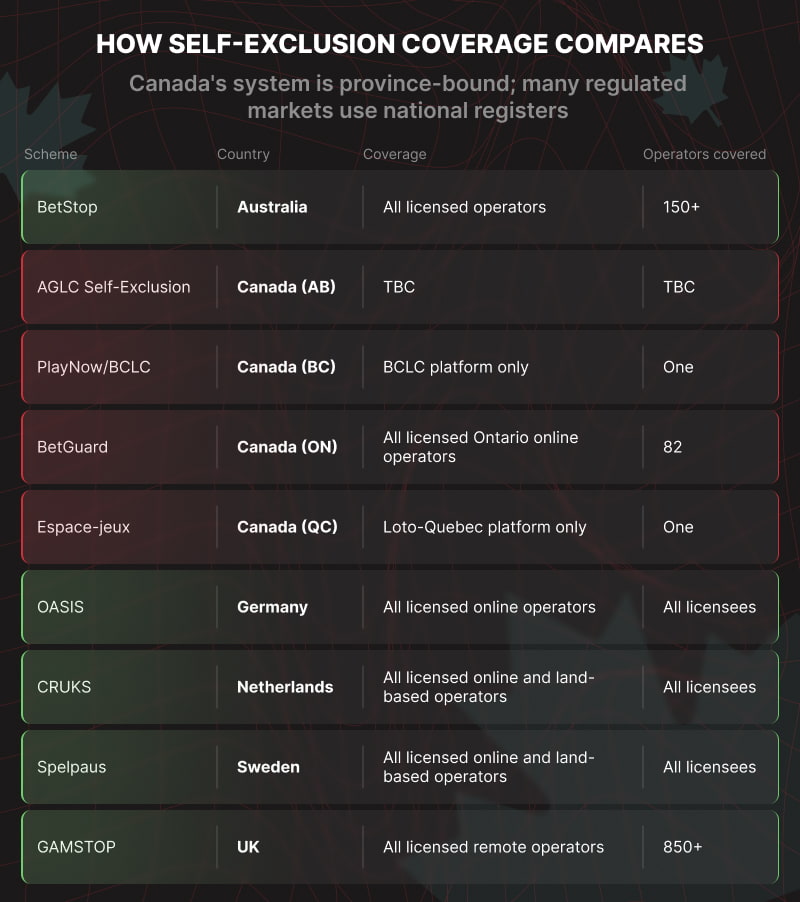

The result is ten parallel regimes, all operating at different standards. Ontario operates an open market, and Alberta is building a similar structure. Every other province runs a government monopoly: BCLC’s PlayNow, Loto-Quebec’s Espace-jeux, and the Atlantic Lottery Corporation.

The issue is that there is no connection between these. A responsible gambling tool in one province has no power in another. A self-exclusion registered in Ontario does not block a player from gambling elsewhere.

Changes do not appear to be on the horizon, with no federal legislation on those issues currently before Parliament.

The Offshore Risks

The Blask 2025 USA and Canada iGaming Landscape Report highlights the scale of this problem. Saskatchewan carries an estimated 93% offshore leakage rate. Alberta and Manitoba sit at 88%. Quebec, where Loto-Quebec has operated since 2010, holds only around 17% of a market estimated at CAD 2.3 billion.

Even British Columbia, with years of PlayNow operations behind it, retains approximately 49-51% of its online market, according to Blask’s reports. Offshore platforms grew at 40% year-on-year in 2025, nearly double the 23% growth of domestic licensed operators.

Ontario’s Success and Limits

Ontario deserves genuine credit for its current position, and it is often hailed as an example of a strong regulatory market.

The regulated market generated CAD 82.7 billion in wagers and CAD 2.9 billion in gross gaming revenue in FY2024/25. Channelisation, measured by the share of online gamblers using regulated platforms, reached 83.7% in early 2025 and 91.1% on the most recent IPSOS survey.

However, the Ontario story is often viewed as the national story, and this is not the case. Even within the province, 20.2% of players using regulated platforms also gamble on unregulated sites.

BetGuard, launched in May 2026, finally delivered the centralised self-exclusion system that the market should have had from day one, allowing a player to exclude from all regulated platforms at once.

The early take-up numbers show more than 500 people registered for BetGuard in its first two weeks. That is not a negligible start, and iGaming Ontario has stated it will measure the platform’s success by renewal rates, term lengths selected, and connections to addiction support services.

However, Ontario’s market has 1.235 million active player accounts. The gap between the scale of the regulated market and the early uptake of the tool is wide.

The deeper problem is that BetGuard is province-bound. A player who is excluded in Ontario is not blocked elsewhere.

Many other countries have solved this problem. GAMSTOP in the UK covers all licensed remote operators under a single registration. Spelpaus in Sweden does the same across online and land-based channels. BetStop in Australia covers approximately 150 licensed wagering providers with a five-minute sign-up.

Canada has no equivalent, and there is currently no route to making one.

What the Evidence Says

The academic case for nationally coordinated self-exclusion is strong. A comparative review of self-exclusion programmes across multiple jurisdictions found that the reach and enforcement of any scheme vary directly with how completely it covers the market.

A review of BCLC’s voluntary self-exclusion programme found that 97% of participants who gambled while excluded did so at venues not covered by their agreement. The exclusion worked where it applied, but not beyond that.

The tool-uptake literature is equally sobering. Studies analysing voluntary deposit-limit setting across large player populations find uptake rates in the low single digits over three-month periods. Ontario does not publish equivalent figures, but iGO’s own Leger survey in 2024 found that only 65.4% of regulated players were aware of available RG tools.

The gap between knowing a tool exists and using it is consistently wide, and no regulator publishes data on actual tool engagement rates. That absence is itself a significant accountability problem.

Where public health data does exist, it is alarming. British Columbia’s 2025/26 prevalence study found that 35% of past-year online gamblers showed moderate or high-risk behaviour.

The most striking recent evidence comes from a January 2026 CMAJ study analysing contacts with Ontario’s ConnexOntario helpline over thirteen years.

The study found that gambling-related contacts increased from a monthly rate of 13.4 per million before online gambling launched, to 17.0 after PlayOLG’s introduction, to 26.2 following the market opening in April 2022.

The increases occurred almost exclusively in adolescent boys and men aged 15 to 44, with the 15-to-24 age group estimated to have seen contacts rise by 337.8%.

A regulated market that generates record-breaking wagers and a near-200% increase in gambling-related helpline contacts simultaneously is simply demonstrating that market growth and player protection are not the same thing.

The Future

Alberta’s launch will introduce centralised self-exclusion from day one, requiring all registered operators to integrate with AGLC’s self-exclusion programme as a condition of registration.

This is a huge step in the right direction, but, like BetGuard, it will still be province-bound.

The case for a shared register is strong. Licensed operators are also competing with offshore threats. A functioning national self-exclusion infrastructure, combined with the channelisation benefits that a well-regulated market delivers, serves their commercial interests as directly as it serves players’ welfare.

If Canada is going to solve its responsible gambling issues, it needs to admit that the fragmented framework has shortcomings in customer care and stop using Ontario’s success as a stand-in for the country as a whole.

The post Canada’s Safer Gambling Gap: Why Market Success Doesn’t Always Equal Player Safety appeared first on Americas iGaming & Sports Betting News.

-

10bet5 days ago

10bet5 days agoEllis Park Stadium signs five-year naming rights deal with 10bet

-

central asia5 days ago

Groove confirms attendance at SBC Summit Tbilisi 2026

-

Bucharest4 days ago

Eeze opens 1,200 sqm Bucharest hub for technical teams

-

API integration3 days ago

Belatra signs cooperation deal to distribute slots via VeliGames

-

Caesars Rewards7 days ago

Raise a Glass: The Vanderpump Hotel Celebrates $813,553 Jackpot Win

-

affiliate marketing4 days ago

SEOBROTHERS’ Aleksandra Drigo flags higher barriers for affiliates in regulated Alberta

-

Compliance Updates5 days ago

KSA Updates Guidelines for Conducting Means Test

-

Big Bass Blast5 days ago

Pragmatic Play adds Big Bass Blast to Big Bass slot series