Canada

Exclusive Q&A w/ Julian Borg-Barthet, Chief Commercial Officer at Lady Luck Games

You recently made your LatAm debut in Mexico with operator LoGrand Entertainment. What makes Mexico the ideal market for your suite of slot games?

Mexico is a thriving online casino market where regulations are stringent when it comes to player protection while still ensuring it is commercially viable for operators and game studios. There is a strong appetite for engaging and entertaining online casino and slot content among a wide range of player audiences, and, as a studio with bold and ambitious plans for the wider LatAm market, we wanted to be among the first to deploy games in Mexico. Our partnership with LoGrand Entertainment is a testament to the quality of our slots with the operator sharing our belief and confidence that they will hit the mark with players. We are also soon live with Cbet – another tier-one LatAm operator – and the feedback we have received from both operators and their players has been incredible. Titles such as Weight of the Gun, Mr. Alchemister, and Ruler of Egypt have quickly risen to the top of the charts – so too have those that use our innovative pipe mechanic. These are unique, one-reel slots that have really taken the market by storm.

We see Mexico very much as the foundation for building our presence across Latin America and we will continue to enter additional markets as regulations allow. Across the continent, online gambling is growing at a rapid rate – in 2021 alone, revenues increased by $7.2bn with no signs of this slowing down as more countries embrace regulation and licensing, allowing operators and studios such as Lady Luck Games to address more of the 400 million people that live in Latin America.

What are players in Mexico and more broadly across LatAm looking for in an online slot? Does this differ from other global markets? If so, how?

The Mexican market is broken down as follows – 60% is sports betting and 40% is online casino games such as slots, blackjack, poker, and lottery. Lady Luck Games is focused entirely on the casino vertical and is on a mission to bring top-quality content to players in markets across Latin America. This is already a highly competitive market and the quality of the experience offered by operators will ultimately determine the level of success they achieve. Player expectations are high, and they absolutely must be met and where possible, exceeded. An online casino lives or dies based on the games offered to players, and we want our operator partners to be able to provide a lobby of slots that players keep coming back to. To date, we have launched slots from our international portfolio that we believe offer what players are looking for, but we are now gathering data and feedback which will be used to develop games specifically for the market, allowing operators to truly localise their slot portfolios. In Mexico, this means exploring games around themes such as Inca, Dia de Los Muertos, and Piñatas.

Can you tell us more about your plans for Latin America? What makes it such an attractive market for Lady Luck?

We are keeping a very close eye on how regulations progress in various countries across the region and are always considering the best opportunities for Lady Luck Games to explore. Colombia is certainly on the agenda as well as countries that have regulated or are regulating online gambling. Markets that have gone down this path such as Buenos Aires (Argentina) are seeing significant yet stable growth and this really should make other jurisdictions sit up and take note. All eyes are currently on Brazil – the sleeping giant of Latin America – as legislation getting over the line here would be a game changer. Retail gambling is prohibited but online gambling is grey and some brands are actively targeting the market and building sizable player bases that they will be able to really maximise as and when enabling law is passed. As for Lady Luck, we plan to be in all regulated online casino markets that are commercially viable.

Where is the opportunity greater – North or South America? Why?

This is a really interesting question. If you just look at the size of the addressable market and the predicted GGR from each, North America has the edge. But when you factor in things like licensing, the need to secure market access partnerships and the incredibly high cost of marketing and brand-building, then the scales could tip in the other direction. Either way, it’s safe to say that both markets provide tremendous opportunities for operators and game developers to explore and that’s exactly what we are doing in both North and South America.

How is your licence application in Ontario progressing? What impact will your games have on the market?

We took the decision to postpone our application for an Ontario licence due to our acquisition of ReelRNG and the launch of our new remote game server, StormRGS. Now that this is live, we plan to pick up our Ontario licence application once again this year. We have already received strong feedback from Ontario operators when we presented at CGA last year, so we are determined to make our full suite of games available to all operators targeting the market as soon as possible and to see how players respond to our striking animations, powerful sound, big bonuses, and action-packed gameplay.

Do you have any plans to make a move in the US? Which states in particular are on your radar?

We are keen to make a move in key US online casino states such as New Jersey, Pennsylvania, and Michigan, and these markets are firmly on our roadmap. That said, I doubt we will secure licences and go live in these states this year as we are prioritising Latin America for now while also focusing on the launch of our new state-of-the-art platform for European operators.

What can European developers bring to the table in these markets?

Online casino is incredibly advanced in most European markets. The studios that have focused on Europe are at the cutting edge of online slot development and are the ones bringing innovations and new concepts to players for the first time. It’s still early days for US studios and many are still concentrating on an omnichannel approach by getting back Casino titles online, while European developers are pushing boundaries and creating the next generation of mobile-first casino content. It won’t be long before players in North and South America seek out games that develop these , never seen before experiences, and that will see them fire up the reels on titles created by European studios such as Lady Luck.

Powered by WPeMatico

High 5 Games, the creator of premium casino content for the land based, online and social gaming markets announced it has secured supplier approval from the Alberta Gaming, Liquor and Cannabis Commission (AGLC), extending its games beyond Play Alberta to all licensed operators in the province’s newly opened commercial iGaming market.

High 5 Games has entertained Alberta players since 2024 through Play Alberta, the province’s government operated gaming platform, where titles such as DaVinci DeluxeWays, Billionaire’s Bank, Green Machine and more have become established player favourites. With Alberta’s commercial market now open, that same proven portfolio is available to all licensed operators entering the province.

Alberta’s commercial iGaming market will be opening on July 13, 2026, making it the second Canadian province after Ontario to welcome private sector operators. Overseen by AGLC and the Alberta iGaming Corporation (AiGC), the market launched with nearly 50 registered operator brands, one of the most anticipated regulated market openings in North America this year.

The approval extends High 5 Games’ regulated North American footprint, which includes New Jersey, Michigan, Pennsylvania, Connecticut, West Virginia, Ontario, Quebec, British Columbia. Alberta players will gain access to High 5’s catalogue of player favourite titles, including DaVinci DeluxeWays, Billionaire’s Bank, Green Machine and other titles through launch partnerships with operators.

“Alberta players already know and love our games through Play Alberta, that is a head start no newcomer to this market can claim. With the open market live, every operator in the province can now offer their players the award winning High 5 titles they have been playing for years, from day one.” says Tony Singer, CEO at High 5 Games.

High 5 Games’ content is certified across New Jersey, Michigan, Pennsylvania, Connecticut, West Virginia, Ontario, British Columbia and the studio has developed more than 300 games over three decades of game making.

The post High 5 Games Expands Across Alberta’s Open iGaming Market Following AGLC Supplier Approval appeared first on Americas iGaming & Sports Betting News.

The supplier can now distribute its online casino titles beyond Play Alberta to all licensed operators in the province.

High 5 Games has secured supplier approval from the Alberta Gaming, Liquor and Cannabis Commission (AGLC), allowing the studio to supply its online casino content to all licensed operators in Alberta’s newly opened commercial iGaming market.

The company has been live in the province since 2024 via Play Alberta, the government-operated platform, where it said titles including DaVinci DeluxeWays, Billionaire’s Bank and Green Machine have become player favourites. With the commercial market now open, High 5 Games said the same portfolio can be offered across operators entering Alberta.

Alberta’s commercial iGaming market is set to open on July 13, 2026, becoming Canada’s second province after Ontario to allow private-sector operators. The market is overseen by AGLC and the Alberta iGaming Corporation (AiGC) and launched with nearly 50 registered operator brands, according to the company.

“Alberta players already know and love our games through Play Alberta, that is a head start no newcomer to this market can claim. With the open market live, every operator in the province can now offer their players the award winning High 5 titles they have been playing for years, from day one.” says Tony Singer, CEO at High 5 Games.

High 5 Games said the AGLC approval expands its regulated North American footprint, which it listed as including New Jersey, Michigan, Pennsylvania, Connecticut, West Virginia, Ontario, Quebec and British Columbia. The company said it has developed more than 300 games over three decades.

The post High 5 Games wins AGLC supplier approval ahead of Alberta iGaming launch appeared first on EE Gaming | Global iGaming & Tech Intelligence Hub.

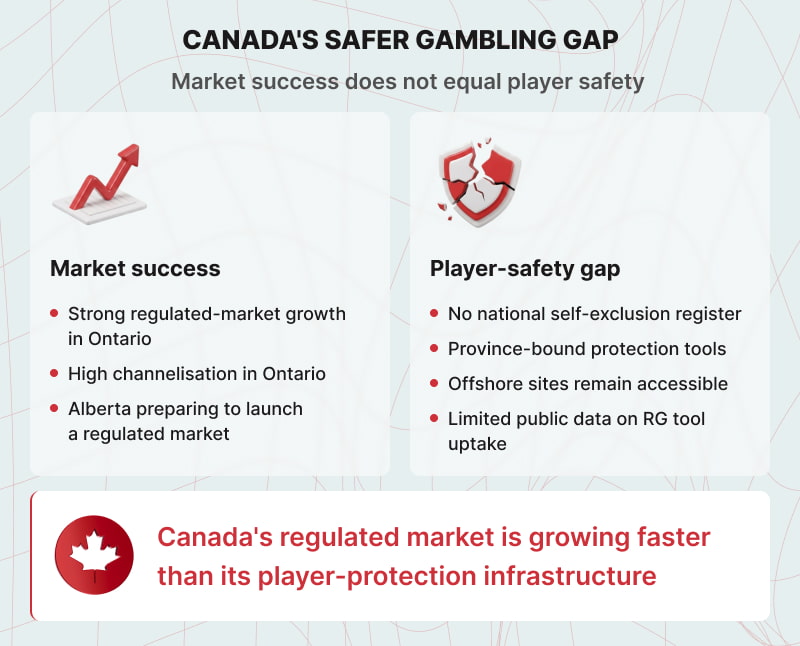

Canada’s online gambling market is the third-largest in the world. It generated approximately CAD 13.15 billion in 2025, growing faster than virtually any other country. By the metrics the industry tends to reach for, it is a success story.

Unfortunately, where many of the metrics that matter for player protection are concerned, the story is different. Unlike several other countries, Canada has no national self-exclusion register and no national licensing framework.

While Ontario is regulated, and there is a lot of excitement around Alberta opening its regulated market this summer, the overwhelming majority of online gambling in the country still happens on unlicensed platforms.

An Ontario or Alberta player who self-excludes still can gamble through offshore sites or outside the province. Canada has no single stop button.

Key Findings

- Canada has no national self-exclusion register, no national licensing framework, and the last national survey predates the legalisation of single-event sports betting.

- Offshore leakage outside Ontario ranges from 49% to 93% by province. The offshore market grew at 40% year-on-year in 2025.

- Ontario has a 91.1% channelisation rate, but 20.2% of players also play on unregulated sites.

- Player awareness of RG tools in Ontario stands at 65.4%, according to iGO’s own Leger survey baseline. No province publishes data on actual tool uptake rates.

- A CMAJ study found gambling helpline contacts in Ontario rose 198% after market privatisation, concentrated almost entirely in men aged 15 to 44.

A Fragmented System

Canada’s gambling framework is a product of its constitution. Sections 91 and 92 of the Constitution Act distribute authority to the provinces, and Section 207 of the Criminal Code permits them to conduct and manage lottery schemes within their own borders. A 1985 federal-provincial agreement completed the transfer, leaving Ottawa without a gambling regulator and the country without national standards of any kind.

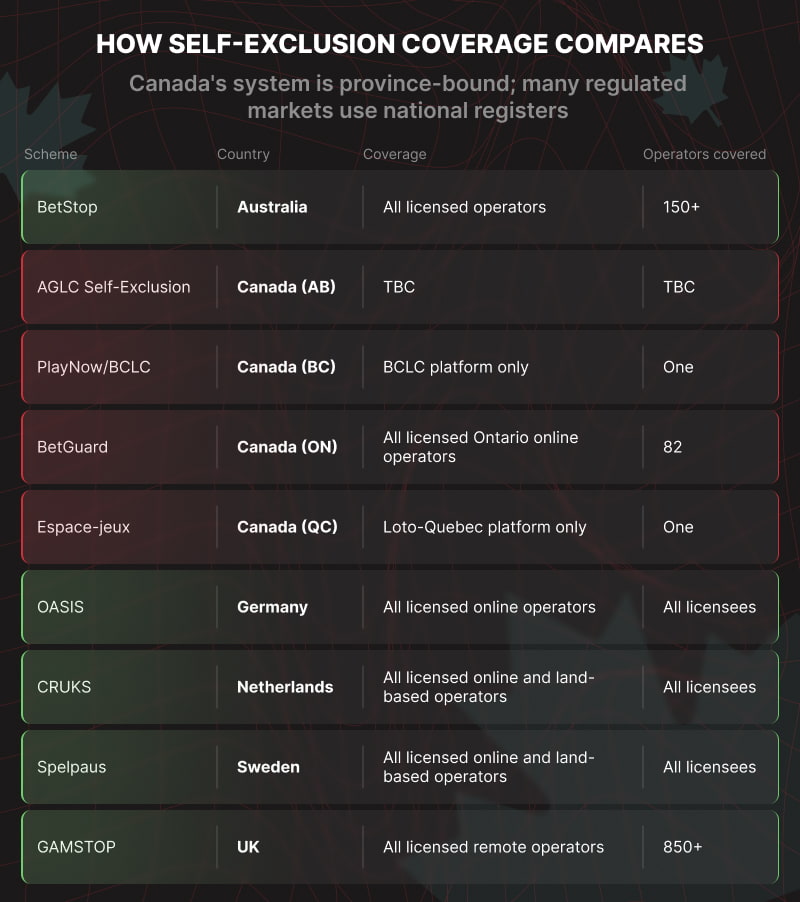

The result is ten parallel regimes, all operating at different standards. Ontario operates an open market, and Alberta is building a similar structure. Every other province runs a government monopoly: BCLC’s PlayNow, Loto-Quebec’s Espace-jeux, and the Atlantic Lottery Corporation.

The issue is that there is no connection between these. A responsible gambling tool in one province has no power in another. A self-exclusion registered in Ontario does not block a player from gambling elsewhere.

Changes do not appear to be on the horizon, with no federal legislation on those issues currently before Parliament.

The Offshore Risks

The Blask 2025 USA and Canada iGaming Landscape Report highlights the scale of this problem. Saskatchewan carries an estimated 93% offshore leakage rate. Alberta and Manitoba sit at 88%. Quebec, where Loto-Quebec has operated since 2010, holds only around 17% of a market estimated at CAD 2.3 billion.

Even British Columbia, with years of PlayNow operations behind it, retains approximately 49-51% of its online market, according to Blask’s reports. Offshore platforms grew at 40% year-on-year in 2025, nearly double the 23% growth of domestic licensed operators.

Ontario’s Success and Limits

Ontario deserves genuine credit for its current position, and it is often hailed as an example of a strong regulatory market.

The regulated market generated CAD 82.7 billion in wagers and CAD 2.9 billion in gross gaming revenue in FY2024/25. Channelisation, measured by the share of online gamblers using regulated platforms, reached 83.7% in early 2025 and 91.1% on the most recent IPSOS survey.

However, the Ontario story is often viewed as the national story, and this is not the case. Even within the province, 20.2% of players using regulated platforms also gamble on unregulated sites.

BetGuard, launched in May 2026, finally delivered the centralised self-exclusion system that the market should have had from day one, allowing a player to exclude from all regulated platforms at once.

The early take-up numbers show more than 500 people registered for BetGuard in its first two weeks. That is not a negligible start, and iGaming Ontario has stated it will measure the platform’s success by renewal rates, term lengths selected, and connections to addiction support services.

However, Ontario’s market has 1.235 million active player accounts. The gap between the scale of the regulated market and the early uptake of the tool is wide.

The deeper problem is that BetGuard is province-bound. A player who is excluded in Ontario is not blocked elsewhere.

Many other countries have solved this problem. GAMSTOP in the UK covers all licensed remote operators under a single registration. Spelpaus in Sweden does the same across online and land-based channels. BetStop in Australia covers approximately 150 licensed wagering providers with a five-minute sign-up.

Canada has no equivalent, and there is currently no route to making one.

What the Evidence Says

The academic case for nationally coordinated self-exclusion is strong. A comparative review of self-exclusion programmes across multiple jurisdictions found that the reach and enforcement of any scheme vary directly with how completely it covers the market.

A review of BCLC’s voluntary self-exclusion programme found that 97% of participants who gambled while excluded did so at venues not covered by their agreement. The exclusion worked where it applied, but not beyond that.

The tool-uptake literature is equally sobering. Studies analysing voluntary deposit-limit setting across large player populations find uptake rates in the low single digits over three-month periods. Ontario does not publish equivalent figures, but iGO’s own Leger survey in 2024 found that only 65.4% of regulated players were aware of available RG tools.

The gap between knowing a tool exists and using it is consistently wide, and no regulator publishes data on actual tool engagement rates. That absence is itself a significant accountability problem.

Where public health data does exist, it is alarming. British Columbia’s 2025/26 prevalence study found that 35% of past-year online gamblers showed moderate or high-risk behaviour.

The most striking recent evidence comes from a January 2026 CMAJ study analysing contacts with Ontario’s ConnexOntario helpline over thirteen years.

The study found that gambling-related contacts increased from a monthly rate of 13.4 per million before online gambling launched, to 17.0 after PlayOLG’s introduction, to 26.2 following the market opening in April 2022.

The increases occurred almost exclusively in adolescent boys and men aged 15 to 44, with the 15-to-24 age group estimated to have seen contacts rise by 337.8%.

A regulated market that generates record-breaking wagers and a near-200% increase in gambling-related helpline contacts simultaneously is simply demonstrating that market growth and player protection are not the same thing.

The Future

Alberta’s launch will introduce centralised self-exclusion from day one, requiring all registered operators to integrate with AGLC’s self-exclusion programme as a condition of registration.

This is a huge step in the right direction, but, like BetGuard, it will still be province-bound.

The case for a shared register is strong. Licensed operators are also competing with offshore threats. A functioning national self-exclusion infrastructure, combined with the channelisation benefits that a well-regulated market delivers, serves their commercial interests as directly as it serves players’ welfare.

If Canada is going to solve its responsible gambling issues, it needs to admit that the fragmented framework has shortcomings in customer care and stop using Ontario’s success as a stand-in for the country as a whole.

The post Canada’s Safer Gambling Gap: Why Market Success Doesn’t Always Equal Player Safety appeared first on Americas iGaming & Sports Betting News.

-

10bet5 days ago

10bet5 days agoEllis Park Stadium signs five-year naming rights deal with 10bet

-

central asia5 days ago

Groove confirms attendance at SBC Summit Tbilisi 2026

-

Bucharest4 days ago

Eeze opens 1,200 sqm Bucharest hub for technical teams

-

API integration3 days ago

Belatra signs cooperation deal to distribute slots via VeliGames

-

affiliate marketing4 days ago

SEOBROTHERS’ Aleksandra Drigo flags higher barriers for affiliates in regulated Alberta

-

Big Bass Blast5 days ago

Pragmatic Play adds Big Bass Blast to Big Bass slot series

-

Compliance Updates5 days ago

KSA Updates Guidelines for Conducting Means Test

-

AB Trav och Galopp2 days ago

BetMakers Technology Group Selected to Distribute ATG Horse Racing Content Across Australia and New Zealand