Canada

Game-Based Learning Market Size is Expected to Surpass $52.8 Billion by 2030 with CAGR of roughly 19.51% | The Future of Learning: Growing Popularity and Trend Based Analysis

Zion Market Research has published a new research report titled “Game-Based Learning Market By End-User (Government, Enterprises, Consumer, Education, And Others), By Revenue Type (Advertising, Game Purchasing, And Others), By Platform (Offline And Online), By Game Type (AI-Based Games, AR/VR Games, Language Learning Games, Assessment & Evaluation Games, And Training Games), And By Region – Global And Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, And Forecasts 2023 – 2030” in its research database.

“According to the latest research study, the demand of global Game-based Learning Market size & share in terms of revenue was valued at USD 10.9 billion in 2022 and it is expected to surpass around USD 52.8 billion mark by 2030, growing at a compound annual growth rate (CAGR) of approximately 19.51% during the forecast period 2023 to 2030.”

What is Game-based Learning? How big is the Game-based Learning Industry?

Report Overview:

The global game-based learning market size was worth around USD 10.9 Billion in 2022 and is predicted to grow to around USD 52.8 Billion by 2030 with a compound annual growth rate (CAGR) of roughly 19.51% between 2023 and 2030.

Game-based learning is a relatively new and modern education approach that makes use of different types of games including online and offline modes to impart knowledge and conduct training sessions. The recent addition of new technology in the larger educational scheme allows learners to engage better and improve the final outcomes of the experience. The industry revolves around the players that deal with the development, design, production, and distribution of products and services related to game-based learning technology.

It comprises simulations, video games, and other types of learning management systems that are game-oriented and can be used in different types of settings including pre-primary to university level. However, the application of game-based learning systems goes beyond educational programs for students and can be applied in corporate or business settings as well for personnel training and skill development. With the advancements in technology, the game-based learning industry is witnessing a high rate of growth and is expected to continue the same trend in the coming years.

Our Free Sample Report Consists of the Following:

- Introduction, Overview, and in-depth industry analysis are all included in the 2023 updated report.

- The COVID-19 Pandemic Outbreak Impact Analysis is included in the package

- About 210+ Pages Research Report (Including Recent Research)

- Provide detailed chapter-by-chapter guidance on Request

- Updated Regional Analysis with Graphical Representation of Size, Share, and Trends for the Year 2023

- Includes Tables and figures have been updated

- The most recent version of the report includes the Top Market Players, their Business Strategies, Sales Volume, and Revenue Analysis

- Zion Market Research research methodology

Global Game-based Learning Market: Growth Factors

The global game-based learning market is projected to grow owing to the increasing demand and preference toward skill development. The teaching community along with students and guardians have realized that working on the development of a specific skill is better for the future of young minds and great emphasis is being laid on the development of technologies that can provide customized or specific learning experiences. Game-based learning tools best fit the modern-age trend. Additionally, the industry is also witnessing immense growth in personalized training since it meets the important set of students’ needs and passion thus aligning both the critical components of overall growth in one set. Students tend to incline more toward learning experiences that work in line with their desire for more flexibility. Moreover, the growing popularity of mobile learning may work in the favor of the industry.

The increasing adoption of smartphones and other mobile devices like tablets and laptops is propelling the demand for online or digital education leading to higher adoption of game-based learning platforms. The fraternity players are expected to generate more revenue owing to the surging adoption of the tools and platform in corporate learning programs as well.

However, the game-based learning industry deals with growth restrictions, especially in terms of limited access to new technology owing to its high cost as well as less awareness rate in emerging economies. Game-based learning tools are expensive due to the complexity of the software programs and the demand for high-priced hardware systems. Furthermore, for the smooth functioning of these tools, the educational unit must have appropriate Information Technology (IT) setup or the industry may fail in achieving its intended goal. In addition to this, the existence of resistance to change and technical issues along with a lack of skilled professionals to deal with issues are other factors working against the market expansion trend.

Report Scope

| Report Attribute | Details |

| Market Size in 2022 | USD 10.9 billion |

| Projected Market Size in 2030 | USD 52.8 billion |

| CAGR Growth Rate | 19.51% CAGR |

| Base Year | 2022 |

| Forecast Years | 2023-2030 |

| Key Market Players | Quizlet, Duolingo, Classcraft, Kahoot!, Udacity, Minecraft Education Edition, Learning Games Network, Edmentum, BrainPOP, Legends of Learning, Nearpod, Schell Games, Rosetta Stone, Coursera, Prodigy Education, edX, TypingClub, Roblox Education, Code.org, Filament Games |

| Key Segment | By End-User, By Revenue Type, By Platform, By Game Type, And By Region |

| Major Regions Covered | North America, Europe, Asia Pacific, Latin America, and the Middle East &, Africa |

| Purchase Options | Request customized purchase options to meet your research needs. |

Game-based Learning Market: Segmentation Analysis

The global game-based learning market is segmented based on end-user, revenue type, platform, game type, and region

Based on end-user, the global market segments are government, enterprises, consumers, education, and others.

Based on revenue type, the game-based learning industry divisions are advertising, game purchasing, and others.

- Game purchasing is expected to witness the highest growth in the industry during the forecast period

- In this revenue model, customers tend to buy the game they wish to invest in and it can either be a one-time payment or based on a subscription, depending on the offerings for the product developer

- In the advertising model, several companies post their advertisements on the platform through which the latter receives revenue for every ad posted. This model is less common in the educational sector due to integrity issues and the constant display of ads can lower the impact of the tool itself

- The annual subscription for Minecraft Education Edition as of 2021 was around USD 5 per user with a minimum purchase of 150 licenses

Based on platform, the global game-based learning market segments are offline and online.

Based on game type, the global market is divided into AI-based games, AR/VR games, language learning games, assessment & evaluation games, and training games.

- Language learning games are the most popular as of recent timeline and their popularity is driven due to their capacity to assist in teaching new language in interactive and immersive ways

- Hence they become more appealing to a larger set of audience

- Assessment and evaluation games work better to understand the skill level developed by the learner after sufficient use of the tool. These tools work best in case there is a need to identify skill gaps and potential room for improvement

- Although subjective, the average time taken to learn professional-level Mandarin is around 2200 hours of study

The global Game-based Learning market is segmented as follows:

By End-User

- Government

- Enterprises

- Consumer

- Education

- Others

By Revenue Type

- Advertising

- Game Purchasing

- Others

By Platform

- Offline

- Online

By Game Type

- AI-Based Games

- AR/VR Games

- Language Learning Games

- Assessment & Evaluation Games

- Training Games

Competitive Landscape

Some of the main competitors dominating the global Game-based Learning market include –

- Quizlet

- Duolingo

- Classcraft

- Kahoot!

- Udacity

- Minecraft Education Edition

- Learning Games Network

- Edmentum

- BrainPOP

- Legends of Learning

- Nearpod

- Schell Games

- Rosetta Stone

- Coursera

- Prodigy Education

- edX

- TypingClub

- Roblox Education

- Code .org

- Filament Games

Key Insights from Primary Research:

- According to the analysis shared by our research forecaster, the Game-based Learning market is likely to expand at a CAGR of around 19.51% during the forecast period (2023-2030).

- In terms of revenue, the Game-based Learning market size was valued at around US$ 10.9 billion in 2022 and is projected to reach US$ 52.8 billion by 2030.

- The game-based learning market is projected to grow at a significant rate due to the growing application of technology in the education sector

- Based on platform segmentation, online was predicted to show maximum market share in the year 2022

- Based on end-user segmentation, education was the leading user in 2022

- On the basis of region, North America was the leading revenue generator in 2022

Key questions answered in this report:

- What is the market size and growth rate forecast for Game-based Learning industry?

- What are the main driving factors propelling the Game-based Learning Market forward?

- What are the leading companies in the Game-based Learning Industry?

- What segments does the Game-based Learning Market cover?

- How can I receive a free copy of the Game-based Learning Market sample report and company profiles?

Key Offerings:

- Market Size & Forecast by Revenue | 2023−2030

- Market Dynamics – Leading Trends, Growth Drivers, Restraints, and Investment Opportunities

- Market Segmentation – A detailed analysis By End-User, By Revenue Type, By Platform, By Game Type, And By Region

- Competitive Landscape – Top Key Vendors and Other Prominent Vendors

Regional Analysis:

The global game-based learning market is projected to witness the highest growth in North America with the US and Canada dominating the majority of the regional share. The high CAGR is driven by factors like the existence of established and technologically advanced educational infrastructure, growing investments towards the development of new platforms for different end-user verticals, increasing adoption of the product, tools, or systems for corporate or educational training, and availability of high disposable income to spend on new learning systems. Growth in Europe may be driven by the rising initiatives of the government to upgrade educational programs by utilizing digital systems and tools along with favorable policies promoting skill development. The growing cultural acceptance in Europe may act as a crucial growth propeller.

By Region

- North America

- U.S.

- Canada

- Rest of North America

- Europe

- France

- UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Recent Developments

- In January 2022, Microsoft announced a new addition to the Minecraft Education edition in form of a Chemistry update for better learning of chemistry concepts

- In August 2021, the industry witnessed the launch of Legends Connect by Legends of Learning allowing teachers and students to collaborate seamlessly

- In September 2021, Kahoot! announced the launch of Kahoot! Academy where teachers can access upgraded and high-quality content for game-based learning

Powered by WPeMatico

High 5 Games, the creator of premium casino content for the land based, online and social gaming markets announced it has secured supplier approval from the Alberta Gaming, Liquor and Cannabis Commission (AGLC), extending its games beyond Play Alberta to all licensed operators in the province’s newly opened commercial iGaming market.

High 5 Games has entertained Alberta players since 2024 through Play Alberta, the province’s government operated gaming platform, where titles such as DaVinci DeluxeWays, Billionaire’s Bank, Green Machine and more have become established player favourites. With Alberta’s commercial market now open, that same proven portfolio is available to all licensed operators entering the province.

Alberta’s commercial iGaming market will be opening on July 13, 2026, making it the second Canadian province after Ontario to welcome private sector operators. Overseen by AGLC and the Alberta iGaming Corporation (AiGC), the market launched with nearly 50 registered operator brands, one of the most anticipated regulated market openings in North America this year.

The approval extends High 5 Games’ regulated North American footprint, which includes New Jersey, Michigan, Pennsylvania, Connecticut, West Virginia, Ontario, Quebec, British Columbia. Alberta players will gain access to High 5’s catalogue of player favourite titles, including DaVinci DeluxeWays, Billionaire’s Bank, Green Machine and other titles through launch partnerships with operators.

“Alberta players already know and love our games through Play Alberta, that is a head start no newcomer to this market can claim. With the open market live, every operator in the province can now offer their players the award winning High 5 titles they have been playing for years, from day one.” says Tony Singer, CEO at High 5 Games.

High 5 Games’ content is certified across New Jersey, Michigan, Pennsylvania, Connecticut, West Virginia, Ontario, British Columbia and the studio has developed more than 300 games over three decades of game making.

The post High 5 Games Expands Across Alberta’s Open iGaming Market Following AGLC Supplier Approval appeared first on Americas iGaming & Sports Betting News.

The supplier can now distribute its online casino titles beyond Play Alberta to all licensed operators in the province.

High 5 Games has secured supplier approval from the Alberta Gaming, Liquor and Cannabis Commission (AGLC), allowing the studio to supply its online casino content to all licensed operators in Alberta’s newly opened commercial iGaming market.

The company has been live in the province since 2024 via Play Alberta, the government-operated platform, where it said titles including DaVinci DeluxeWays, Billionaire’s Bank and Green Machine have become player favourites. With the commercial market now open, High 5 Games said the same portfolio can be offered across operators entering Alberta.

Alberta’s commercial iGaming market is set to open on July 13, 2026, becoming Canada’s second province after Ontario to allow private-sector operators. The market is overseen by AGLC and the Alberta iGaming Corporation (AiGC) and launched with nearly 50 registered operator brands, according to the company.

“Alberta players already know and love our games through Play Alberta, that is a head start no newcomer to this market can claim. With the open market live, every operator in the province can now offer their players the award winning High 5 titles they have been playing for years, from day one.” says Tony Singer, CEO at High 5 Games.

High 5 Games said the AGLC approval expands its regulated North American footprint, which it listed as including New Jersey, Michigan, Pennsylvania, Connecticut, West Virginia, Ontario, Quebec and British Columbia. The company said it has developed more than 300 games over three decades.

The post High 5 Games wins AGLC supplier approval ahead of Alberta iGaming launch appeared first on EE Gaming | Global iGaming & Tech Intelligence Hub.

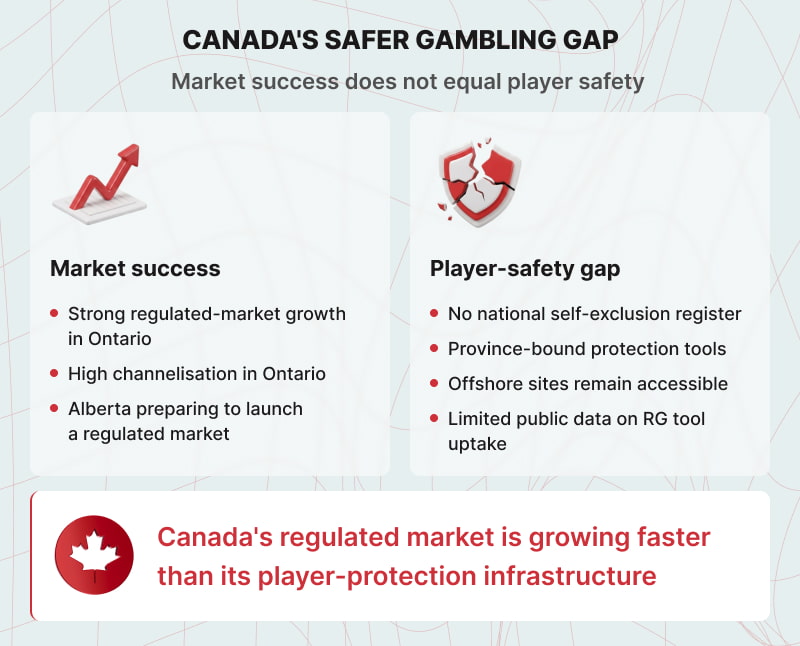

Canada’s online gambling market is the third-largest in the world. It generated approximately CAD 13.15 billion in 2025, growing faster than virtually any other country. By the metrics the industry tends to reach for, it is a success story.

Unfortunately, where many of the metrics that matter for player protection are concerned, the story is different. Unlike several other countries, Canada has no national self-exclusion register and no national licensing framework.

While Ontario is regulated, and there is a lot of excitement around Alberta opening its regulated market this summer, the overwhelming majority of online gambling in the country still happens on unlicensed platforms.

An Ontario or Alberta player who self-excludes still can gamble through offshore sites or outside the province. Canada has no single stop button.

Key Findings

- Canada has no national self-exclusion register, no national licensing framework, and the last national survey predates the legalisation of single-event sports betting.

- Offshore leakage outside Ontario ranges from 49% to 93% by province. The offshore market grew at 40% year-on-year in 2025.

- Ontario has a 91.1% channelisation rate, but 20.2% of players also play on unregulated sites.

- Player awareness of RG tools in Ontario stands at 65.4%, according to iGO’s own Leger survey baseline. No province publishes data on actual tool uptake rates.

- A CMAJ study found gambling helpline contacts in Ontario rose 198% after market privatisation, concentrated almost entirely in men aged 15 to 44.

A Fragmented System

Canada’s gambling framework is a product of its constitution. Sections 91 and 92 of the Constitution Act distribute authority to the provinces, and Section 207 of the Criminal Code permits them to conduct and manage lottery schemes within their own borders. A 1985 federal-provincial agreement completed the transfer, leaving Ottawa without a gambling regulator and the country without national standards of any kind.

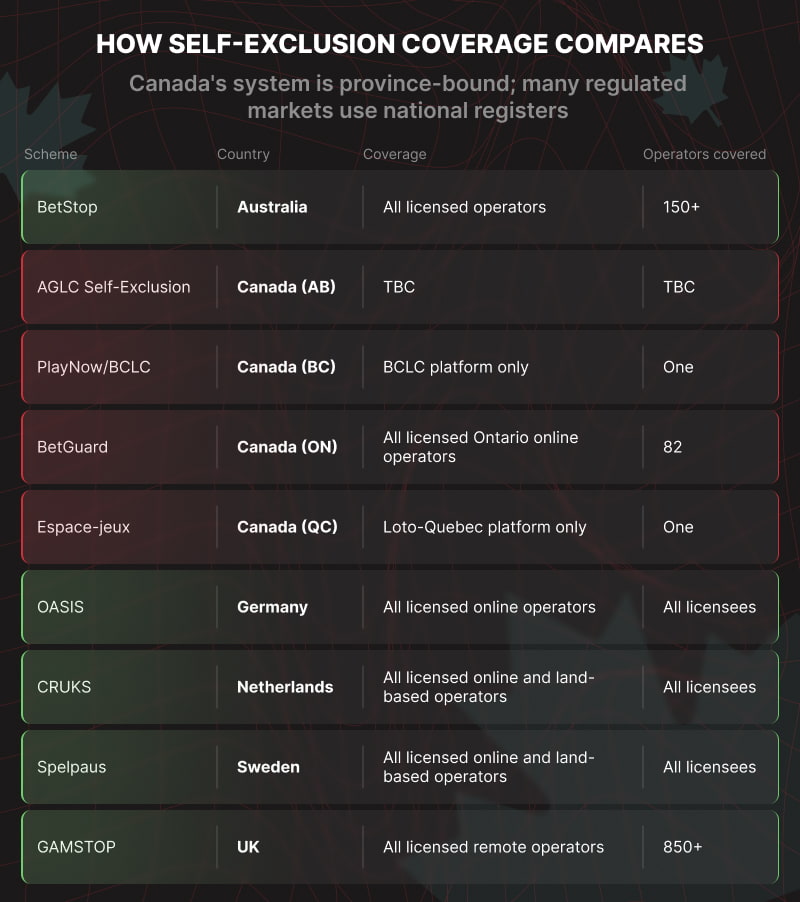

The result is ten parallel regimes, all operating at different standards. Ontario operates an open market, and Alberta is building a similar structure. Every other province runs a government monopoly: BCLC’s PlayNow, Loto-Quebec’s Espace-jeux, and the Atlantic Lottery Corporation.

The issue is that there is no connection between these. A responsible gambling tool in one province has no power in another. A self-exclusion registered in Ontario does not block a player from gambling elsewhere.

Changes do not appear to be on the horizon, with no federal legislation on those issues currently before Parliament.

The Offshore Risks

The Blask 2025 USA and Canada iGaming Landscape Report highlights the scale of this problem. Saskatchewan carries an estimated 93% offshore leakage rate. Alberta and Manitoba sit at 88%. Quebec, where Loto-Quebec has operated since 2010, holds only around 17% of a market estimated at CAD 2.3 billion.

Even British Columbia, with years of PlayNow operations behind it, retains approximately 49-51% of its online market, according to Blask’s reports. Offshore platforms grew at 40% year-on-year in 2025, nearly double the 23% growth of domestic licensed operators.

Ontario’s Success and Limits

Ontario deserves genuine credit for its current position, and it is often hailed as an example of a strong regulatory market.

The regulated market generated CAD 82.7 billion in wagers and CAD 2.9 billion in gross gaming revenue in FY2024/25. Channelisation, measured by the share of online gamblers using regulated platforms, reached 83.7% in early 2025 and 91.1% on the most recent IPSOS survey.

However, the Ontario story is often viewed as the national story, and this is not the case. Even within the province, 20.2% of players using regulated platforms also gamble on unregulated sites.

BetGuard, launched in May 2026, finally delivered the centralised self-exclusion system that the market should have had from day one, allowing a player to exclude from all regulated platforms at once.

The early take-up numbers show more than 500 people registered for BetGuard in its first two weeks. That is not a negligible start, and iGaming Ontario has stated it will measure the platform’s success by renewal rates, term lengths selected, and connections to addiction support services.

However, Ontario’s market has 1.235 million active player accounts. The gap between the scale of the regulated market and the early uptake of the tool is wide.

The deeper problem is that BetGuard is province-bound. A player who is excluded in Ontario is not blocked elsewhere.

Many other countries have solved this problem. GAMSTOP in the UK covers all licensed remote operators under a single registration. Spelpaus in Sweden does the same across online and land-based channels. BetStop in Australia covers approximately 150 licensed wagering providers with a five-minute sign-up.

Canada has no equivalent, and there is currently no route to making one.

What the Evidence Says

The academic case for nationally coordinated self-exclusion is strong. A comparative review of self-exclusion programmes across multiple jurisdictions found that the reach and enforcement of any scheme vary directly with how completely it covers the market.

A review of BCLC’s voluntary self-exclusion programme found that 97% of participants who gambled while excluded did so at venues not covered by their agreement. The exclusion worked where it applied, but not beyond that.

The tool-uptake literature is equally sobering. Studies analysing voluntary deposit-limit setting across large player populations find uptake rates in the low single digits over three-month periods. Ontario does not publish equivalent figures, but iGO’s own Leger survey in 2024 found that only 65.4% of regulated players were aware of available RG tools.

The gap between knowing a tool exists and using it is consistently wide, and no regulator publishes data on actual tool engagement rates. That absence is itself a significant accountability problem.

Where public health data does exist, it is alarming. British Columbia’s 2025/26 prevalence study found that 35% of past-year online gamblers showed moderate or high-risk behaviour.

The most striking recent evidence comes from a January 2026 CMAJ study analysing contacts with Ontario’s ConnexOntario helpline over thirteen years.

The study found that gambling-related contacts increased from a monthly rate of 13.4 per million before online gambling launched, to 17.0 after PlayOLG’s introduction, to 26.2 following the market opening in April 2022.

The increases occurred almost exclusively in adolescent boys and men aged 15 to 44, with the 15-to-24 age group estimated to have seen contacts rise by 337.8%.

A regulated market that generates record-breaking wagers and a near-200% increase in gambling-related helpline contacts simultaneously is simply demonstrating that market growth and player protection are not the same thing.

The Future

Alberta’s launch will introduce centralised self-exclusion from day one, requiring all registered operators to integrate with AGLC’s self-exclusion programme as a condition of registration.

This is a huge step in the right direction, but, like BetGuard, it will still be province-bound.

The case for a shared register is strong. Licensed operators are also competing with offshore threats. A functioning national self-exclusion infrastructure, combined with the channelisation benefits that a well-regulated market delivers, serves their commercial interests as directly as it serves players’ welfare.

If Canada is going to solve its responsible gambling issues, it needs to admit that the fragmented framework has shortcomings in customer care and stop using Ontario’s success as a stand-in for the country as a whole.

The post Canada’s Safer Gambling Gap: Why Market Success Doesn’t Always Equal Player Safety appeared first on Americas iGaming & Sports Betting News.

-

10bet5 days ago

10bet5 days agoEllis Park Stadium signs five-year naming rights deal with 10bet

-

Bucharest4 days ago

Eeze opens 1,200 sqm Bucharest hub for technical teams

-

central asia5 days ago

Groove confirms attendance at SBC Summit Tbilisi 2026

-

API integration4 days ago

Belatra signs cooperation deal to distribute slots via VeliGames

-

AB Trav och Galopp3 days ago

BetMakers Technology Group Selected to Distribute ATG Horse Racing Content Across Australia and New Zealand

-

BETANO4 days ago

Play’n GO strengthens Latin American presence with Betano Colombia launch

-

affiliate marketing5 days ago

SEOBROTHERS’ Aleksandra Drigo flags higher barriers for affiliates in regulated Alberta

-

Big Bass Blast5 days ago

Pragmatic Play adds Big Bass Blast to Big Bass slot series